Event submissions

Published

This submission belongs to the session b. Information and Complexity of the event 4th International Electronic Conference on Entropy and Its Applications

Published date

20 Nov, 2017

Citation

Edgar Parker, The Relationship between the US Economy’s Information Processing and Absorption Ratios, in Proceedings of 4th International Electronic Conference on Entropy and Its Applications, 21 November–1 December 2017, MDPI: Basel, Switzerland, doi: 10.3390/ecea-4-05013

Share

Email

Facebook

Twitter

LinkedIn

The Relationship between the US Economy’s Information Processing and Absorption Ratios

'%3e%3cpath%20d='M12.6647%2010.9104C12.4176%2010.325%2012.0589%209.7933%2011.6088%209.34485C11.16%208.89511%2010.6283%208.53653%2010.0432%208.28891C10.038%208.28629%2010.0327%208.28498%2010.0275%208.28236C10.8437%207.69282%2011.3743%206.73252%2011.3743%205.64907C11.3743%203.85423%209.92005%202.40002%208.12522%202.40002C6.33038%202.40002%204.87618%203.85423%204.87618%205.64907C4.87618%206.73252%205.40677%207.69282%206.22296%208.28367C6.21772%208.28629%206.21248%208.2876%206.20724%208.29022C5.62031%208.53783%205.09365%208.89287%204.64167%209.34616C4.19192%209.79496%203.83334%2010.3266%203.58573%2010.9117C3.34247%2011.4846%203.21128%2012.0987%203.19925%2012.721C3.1989%2012.735%203.20135%2012.7489%203.20646%2012.7619C3.21157%2012.7749%203.21924%2012.7868%203.22901%2012.7968C3.23877%2012.8068%203.25045%2012.8148%203.26334%2012.8202C3.27623%2012.8256%203.29007%2012.8284%203.30406%2012.8284H4.09012C4.14776%2012.8284%204.19362%2012.7825%204.19493%2012.7262C4.22113%2011.7148%204.62726%2010.7676%205.34519%2010.0497C6.08802%209.30686%207.07452%208.89811%208.12522%208.89811C9.17592%208.89811%2010.1624%209.30686%2010.9052%2010.0497C11.6232%2010.7676%2012.0293%2011.7148%2012.0555%2012.7262C12.0568%2012.7839%2012.1027%2012.8284%2012.1603%2012.8284H12.9464C12.9604%2012.8284%2012.9742%2012.8256%2012.9871%2012.8202C13%2012.8148%2013.0117%2012.8068%2013.0214%2012.7968C13.0312%2012.7868%2013.0389%2012.7749%2013.044%2012.7619C13.0491%2012.7489%2013.0515%2012.735%2013.0512%2012.721C13.0381%2012.0947%2012.9084%2011.4856%2012.6647%2010.9104ZM8.12522%207.90243C7.52388%207.90243%206.95792%207.66793%206.53214%207.24215C6.10636%206.81636%205.87185%206.2504%205.87185%205.64907C5.87185%205.04773%206.10636%204.48177%206.53214%204.05599C6.95792%203.63021%207.52388%203.3957%208.12522%203.3957C8.72655%203.3957%209.29252%203.63021%209.7183%204.05599C10.1441%204.48177%2010.3786%205.04773%2010.3786%205.64907C10.3786%206.2504%2010.1441%206.81636%209.7183%207.24215C9.29252%207.66793%208.72655%207.90243%208.12522%207.90243Z'%20fill='%235D1EE1'/%3e%3c/g%3e%3c/svg%3e)

Edgar Parker 1

1. New York Life Insurance Company, 51 Madison Avenue, New York, NY 10010

Abstract

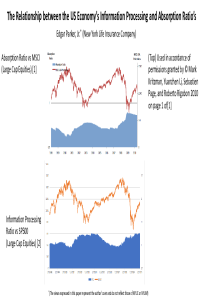

After the 2008 financial collapse, (Kritzman et al 2011) introduced the now popular measure of implied systemic risk called the absorption ratio. This statistic is constructed from a fixed number of eigenvectors, and measures how closely the economy’s markets are coupled. The more closely financial markets are coupled the more susceptible they are to systemic collapse. (Parker 2017) utilized information theory to develop the concept of the entropic yield curve. From this equation, the implied information processing ratio or entropic efficiency of the economy can be derived. This entropic measure can also be useful in predicting economic downturns. In the current work, the relationship between these two ratios is explored.

Keywords

Shannon entropy

Kullback-Leibler divergence

yield curve

volatility

Absorption Ratio

Entropic Yield Curve

Manuscript

sciforum-014674-done.pdf

Poster

Slides -4th International Electronic Conference on Entropy Edgar Parker final.pdf

Sustainability Enhancement of a Biomass Boiler through Exergy Analysis

The irreversibility of the direct and counterflow impinging jet onto profiled heated cavity